A Look Under the Hood

The S&P 500 fell slightly more than the option’s Market Maker Move last week and is now over 10% down from the July high.

Technical Analysis:

The technical picture sure looks ugly as SPY sold off on heavy volume last Wednesday to Friday and even breached the Volume Profile Point of Control. Price is below all moving averages as it failed to bounce above the 200-day simple moving average (red moving average). This leg down may have some more to go, but it is now sitting on a prior congestion area as it is starting to become oversold, as evidenced by the oversold readings on the Slow Stochastics and RSI indicators. The Money Flow Index indicator is also nearing oversold levels and when this indicator shows buying, it could be time for a rally. If selling continues this week, the S2 Pivot Point at $403 is a likely target

The Weak Scenario that we wrote about in a previous article played out as the market continued lower in a downward channel pattern. It did a throw-under below the channel as the Slow Stochastics is oversold. Note that the last time there was a throw-over above the channel with an overbought Stochastics reading, a downtrend to the lower channel line occurred. Its possible its time for a bounce to at least the upper channel line.

If the SPY would fall to the $403 level, it would be a 50% Fibonacci retracement of the October 2022 low to July 2023 uptrend. A possible reversal area.

Under the Hood:

Now let’s try to get a better understanding of what the Big/Smart Money is doing.

Looking at the Commitment of Traders (COT) report for the S&P 500 we could see that Asset Managers are selling, Market Makers (Dealer) are also selling albeit at a lesser degree and Hedge Funds (Lev Money) is buying.

Looking at Long positions, we could see that Asset Managers are actually holding their long positions, as Hedge Funds are increasing their long positions.

It gets interesting when we look at the short positions. Asset Managers are increasing their short positions as they hedge their portfolios. This is probably a significant driver in the recent run-up in the VIX. Dealers are also increasing their short positions, as Hedge Funds take profit on previous short positions.

The NAAIM Exposure Index is a survey of active money managers and Financial Advisors. Typically, when money managers reduce their equity exposure to the 20% mark, the market usually rallies. This is a classic example of “whatever you think the market will do, it does the opposite to create maximum pain”. Financial Advisors are victims of the market makers, just like retail investors. The NAAIM is currently at 24.82. Should the market rally, money managers could find their client portfolios under-allocated to equity and quickly buy equities to chase a new uptrend. This dynamic could provide fuel for a possible year-end rally.

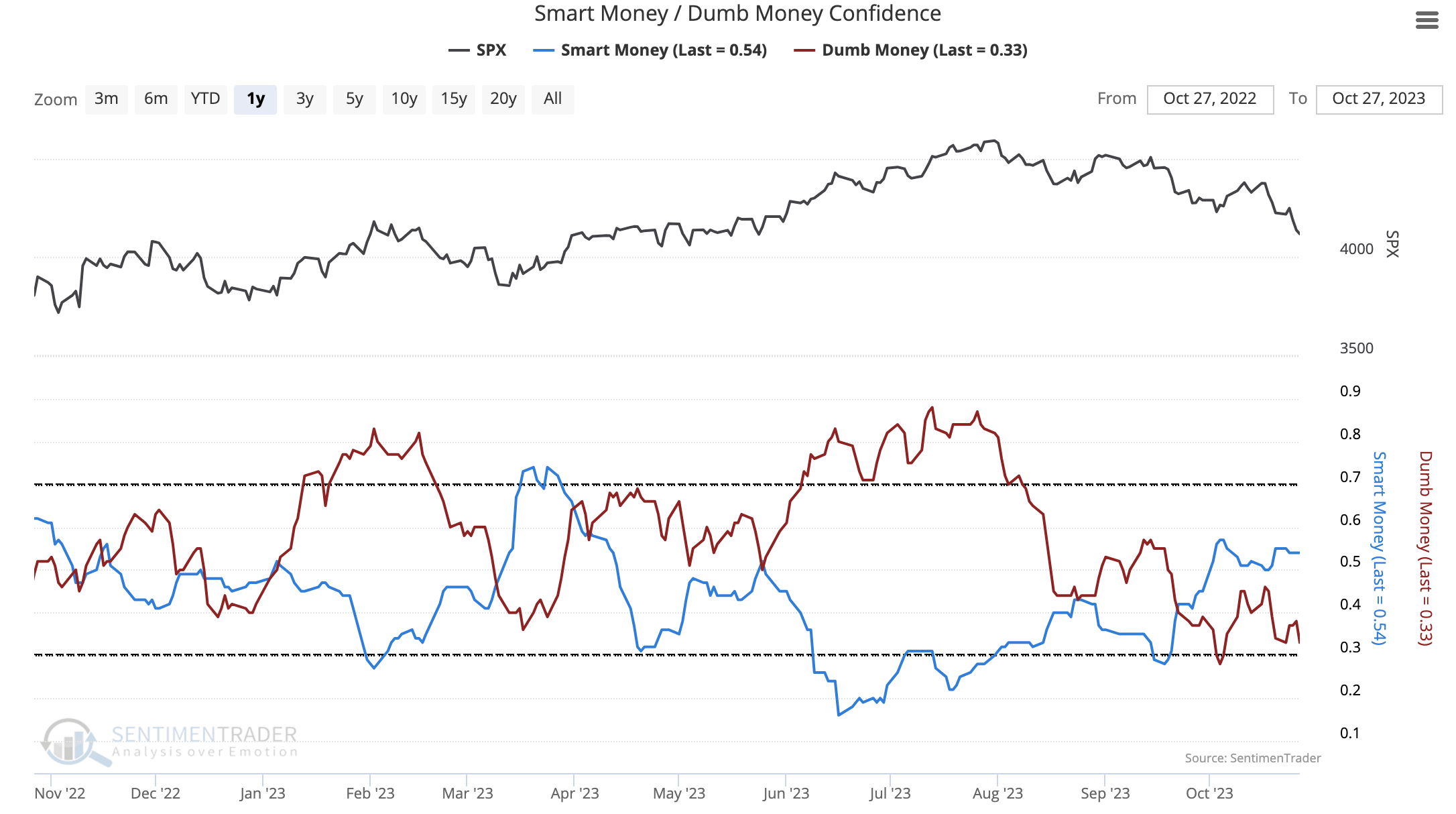

Finally, the Smart Money/Dumb Money Confidence indicator shows that Smart Money is slowly buying the dip as Dumb Money sells in a panic.

Cycles:

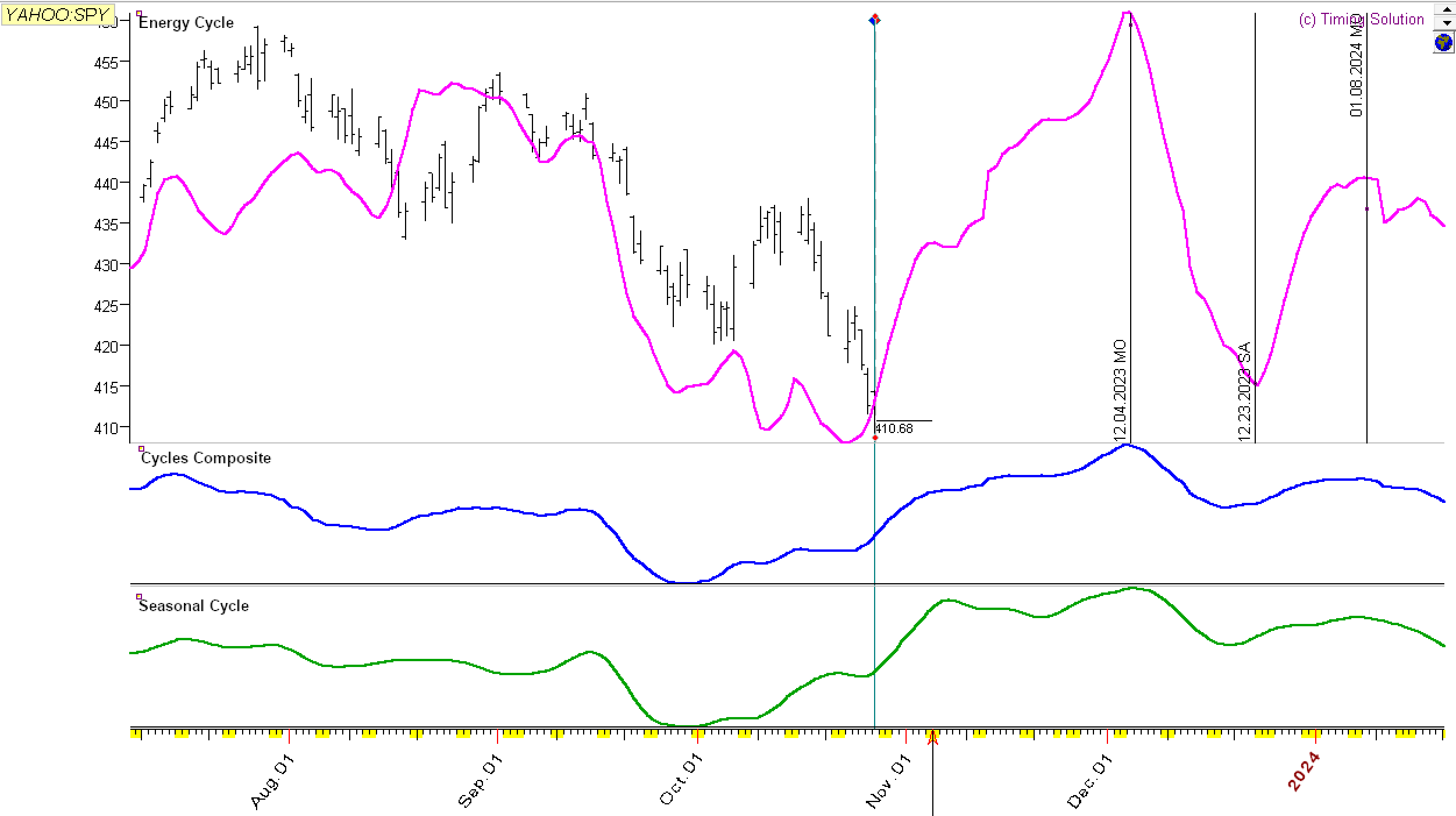

Cycle followers know that cycles usually dictate direction, but not degree. It could be argued that negative macro and geo-political conditions could translate to a weak or late year-end rally. On the bright side, the current oversold conditions and low NAAIM Exposure to equities could be fuel for the uptrend we get when it finally comes. The Energy Cycle below (pink forecast) indicates that the uptrend will occur this week.

As a trader and portfolio manager, before putting my money at risk, I would want to see the SPY catch a trend above the 20 SMA on the hourly chart or the 8 EMA on the daily chart.

Disclaimer - All materials, information, and ideas from Cycles Edge are for educational purposes only and should not be considered Financial Advice. This blog may document actions done by the owners/writers of this blog, thus it should be assumed that positions are likely taken. If this is an issue, please discontinue reading. Cycles Edge takes no responsibility for possible losses, as markets can be volatile and unpredictable, leading to constantly changing opinions or forecasts.