Uranium: THE Asset Of This Decade - Commodity Piece

Introduction To Uranium

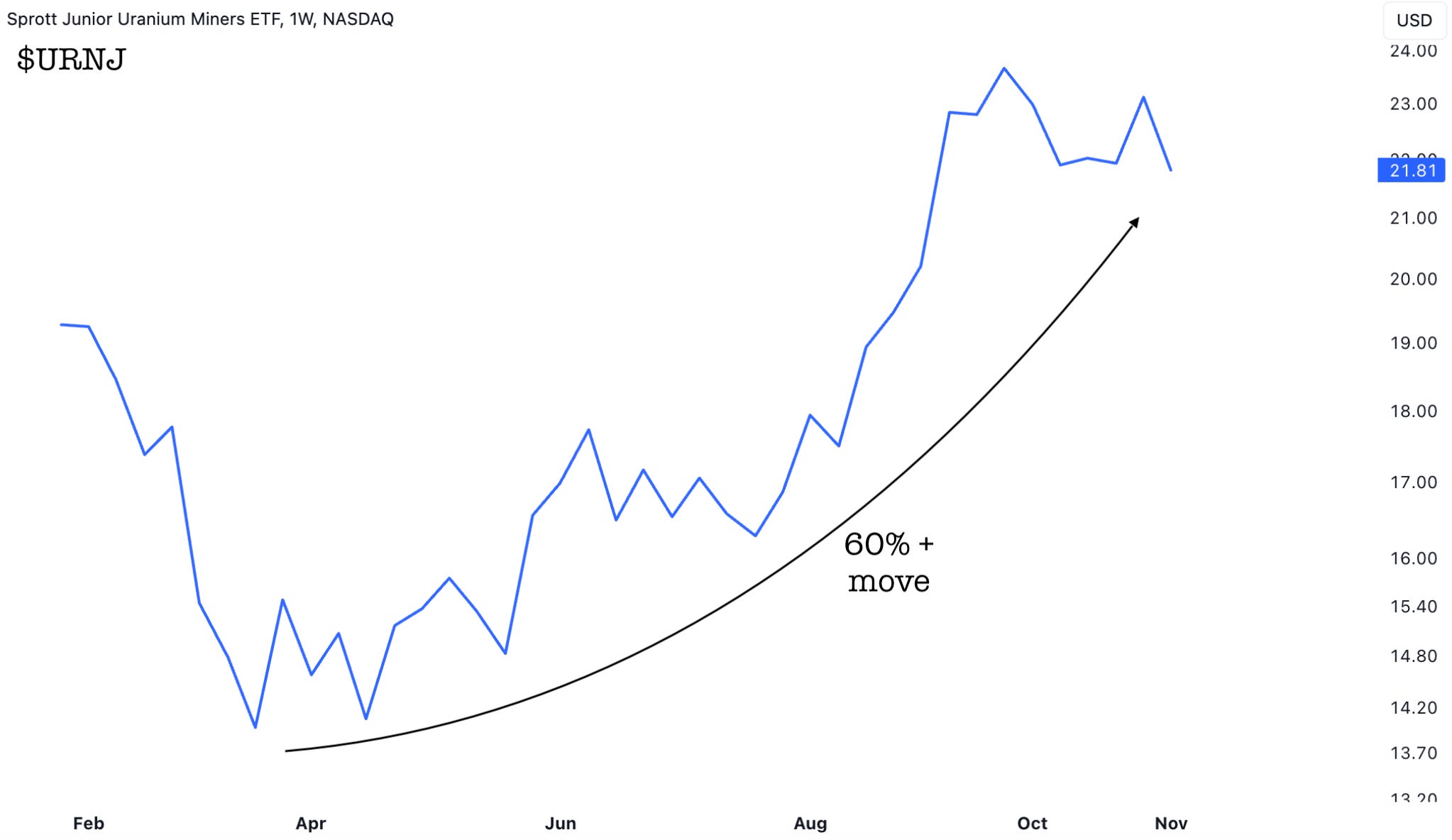

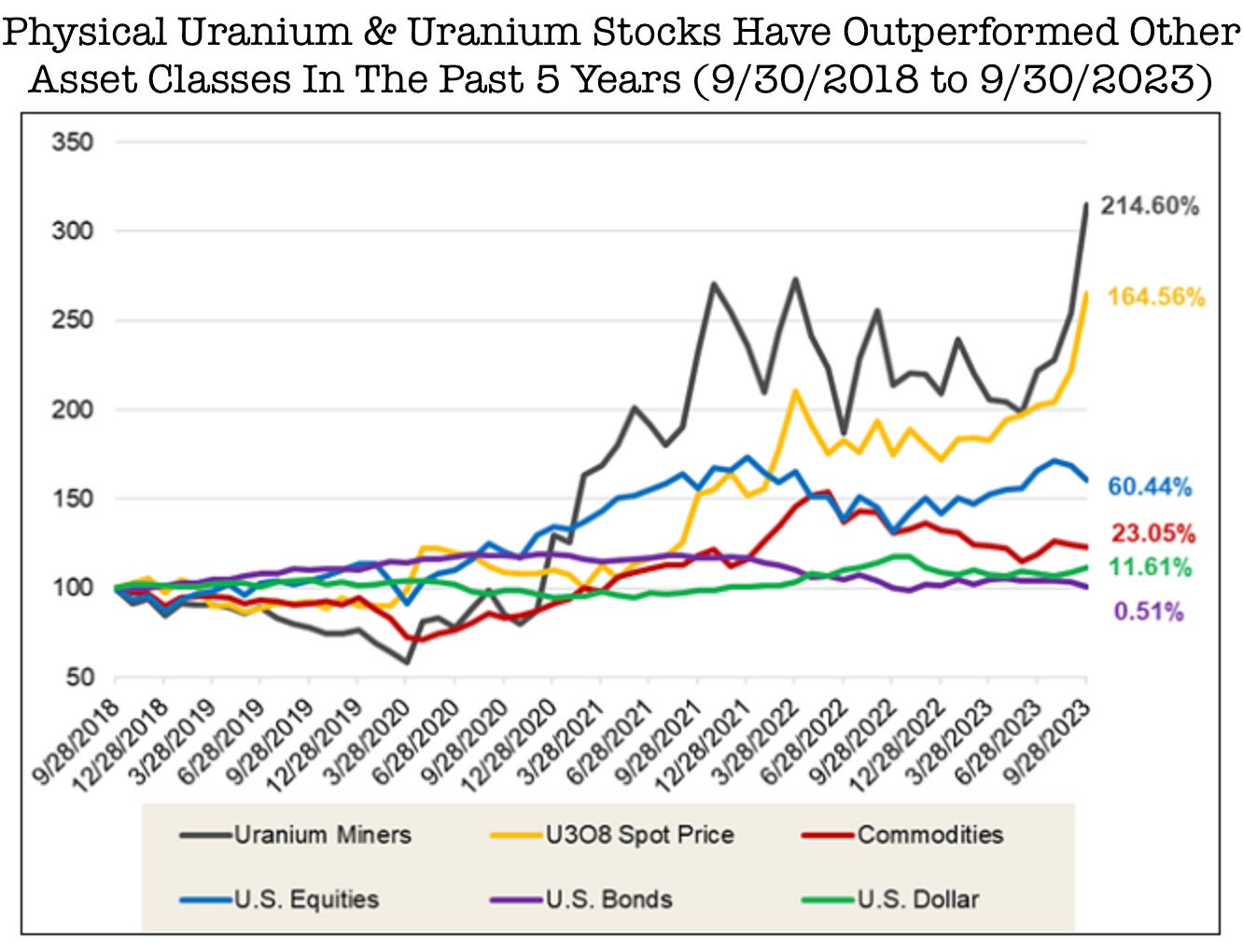

Uranium has gained a lot of attention in 2023 due to a significant price surge. This year alone, uranium miners ($URNM) have experienced a remarkable increase of over 55% from March onwards, while junior uranium miners ($URNJ) have seen a surge of over 60% during the same period.

Uranium plays a crucial role in the production of clean and zero-emission nuclear energy. Nuclear power plants utilize a process called nuclear fission, where a neutron collides with a uranium atom, causing it to split and release a substantial amount of energy in the form of heat and radiation. This chain reaction continues as the neutrons collide with other uranium atoms. Nuclear power plant reactors control this process to generate the desired amount of energy.

Nuclear energy can also be produced through nuclear fusion, which involves combining or fusing atoms to form a larger atom. Fusion is the energy source of the sun and stars. While research on harnessing nuclear fusion as a source of energy is ongoing, its commercial viability remains uncertain due to the challenges of controlling a fusion reaction.

The advantages of nuclear energy include:

Cleanliness: CO2 emissions comparable to renewables

Reliability: Provides reliable baseload energy to offset intermittency from increasing renewable energy sources

Efficiency: High energy density

Safety: Impeccable long-term safety record is gaining worldwide acceptance

There are 3 naturally occurring isotopes of uranium:

Uranium-238 - The heaviest and most abundant

Uranium-235

Uranium-234

Uranium-235 is the only type that undergoes fission. Uranium ore concentrate, known as U3O8 or yellowcake, is created through chemical processing of uranium ore. The resulting fine powder is packaged in steel drums and sent to refineries for further processing to prepare it as fuel for nuclear reactors.

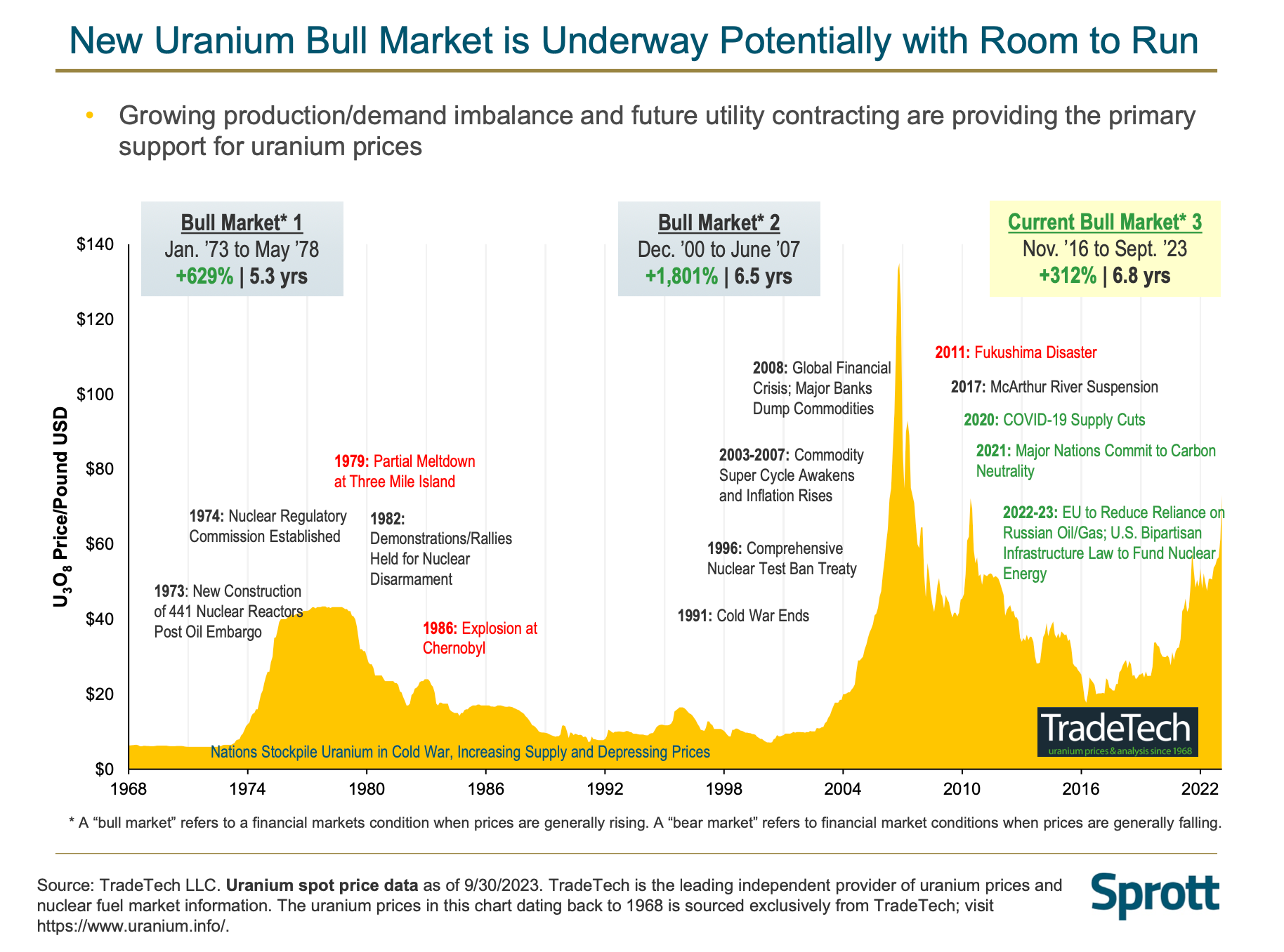

U3O8 (UX1! on Tradingview) has seen a remarkable surge of over 300% since 2017 and has risen by more than 50% since the beginning of 2023. Additionally, uranium is displaying promising signs from a fundamental perspective, making it an attractive asset class for this decade.

7 Key Drivers Igniting Uranium’s Revival

Higher Uranium Demand Forecasts

The World Nuclear Association's (WNA) latest report reveals a stunning forecast - uranium demand is set to nearly double by 2040. Notably, this surge is fueled by the inclusion of Small Modular Reactors (SMRs), a game-changing technology.

Demand From Small Modular Reactors (SMRs)

SMRs are revolutionizing the nuclear energy landscape. The International Atomic Energy Agency (IAEA) characterizes small reactors as those with a capacity of up to 300 MW(e) per unit — roughly a third of conventional nuclear reactors' size. The modular design of SMRs means components can be manufactured in factories and transported for on-site assembly, reducing costs and construction time. This adaptability positions SMRs to deliver clean energy to areas that were previously out of reach for conventional nuclear plants.

Long-Term Contracting Surge

Utilities and uranium producers generally contract in the term market, representing uranium sold under long-term, multi-year contracts with deliveries starting 1 to 3 years after the agreement is finalized. By contrast, a spot market contract is generally for a single delivery, which is priced at the time of purchase. Prior to the Russia’s invasion of Ukraine, uranium term contracting was very suppressed for nearly a decade. However, 2022 saw a turnaround with the highest volume of term contracting in a decade at 125 million pounds of U3O8. 2023 year-to-date (as of 31st October) is set to surpass this, with current term contracting at 121 million pounds already.

This increase in uranium term contracting should be viewed against a decade of underinvestment in uranium supply, and decades of mine production that fell below world nuclear reactor requirements. The increased contracting has squeezed the market into a very tight state, and we believe it will continue to push uranium prices higher over the coming years, thus incentivizing new production.

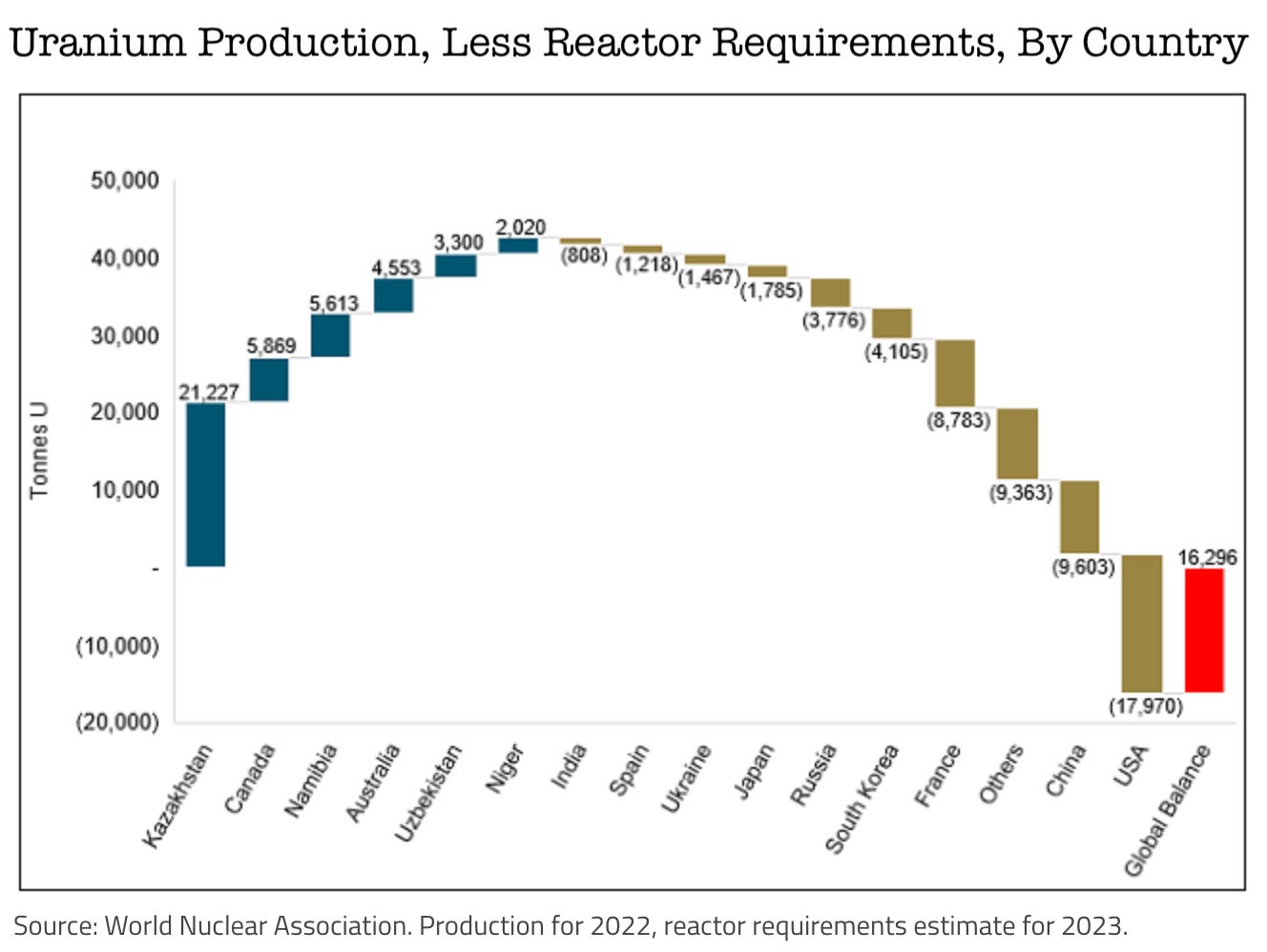

Notably, most term contracting year-to-date has been done by countries outside the U.S. However, U.S. contracting may be a future tailwind as the U.S. needs to replace inventory. Currently, the U.S. depends entirely on sourcing uranium from other countries for what represents the largest reactor requirements in the world, as shown in the figure below.

Supply Uncertainties Intensify

Although the strengthening uranium price is stimulating a supply response, recent developments underscore the complexities of introducing new supply streams. Historically, uranium from Kazakhstan, the world's top producer, was mainly routed through Russia for Western markets. While this transit method persists, potential disruptions loom due to possible sanctions and challenges in shipping and insurance. Given that Kazakhstan accounts for 44% of global U3O8 production, any supply disturbances could profoundly affect the market. Moreover, the coup in Niger this year has drawn international sanctions that has hampered logistics in the country, and forced Orano Imouraren mine to halt uranium processing in Niger.

In the long run, as existing mines are exhausted, the uranium supply will hinge more on the revival of dormant mines and the establishment of new ones. Recent challenges, such as those faced by Cameco and Peninsula Energy in restarting mines, or the delay in Global Atomic's Dasa project in Niger, coupled with the lengthy 8-15 year timeline from discovery to production, underscore the industry's struggle to ramp up uranium output.

Limitations With Alternative Sources

At the European Nuclear Society (ENS) conference in October 2023 it became clear that end-users are also focusing on other sources of supply, as they appear to recognize that primary supply won’t able to meet increasing demand.

Phosphate tails, seawater extraction, increased production from polymetallic mines and several more have been discussed. However, these alternative sources are expensive, time consuming, and present technological challenges. In order for the risk-reward to make sense, higher uranium prices for longer are required.

Extending The Life Of Existing Nuclear Plants And Restarts

Most nuclear power plants have an operating lifetime of 25 to 40 years, but many can be extended to 60 years or, in the US, up to 80 years. For instance, the US's Diablo Canyon nuclear power plant has been in operation since 1985 and was scheduled to close by 2025, but regulators gave an extension to operate for 5 additional years. The extensions of planned operating lifetimes incrementally increases the demand for uranium. The Nuclear Fuel Report by WNA stated that upward of 140 reactors could be subject to extended operations from now until 2040.

Nuclear reactor restarts have also contributed to the increasing demand for uranium. Many countries have now made a U-turn in their nuclear energy policies and are restarting reactors that were closed in the past decade. A prime example of this is Japan, which has restarted 11 nuclear reactors, and another 16 are at various stages in the process of restarting approval, according to WNA. South Korea is another example that has fully reversed its nuclear phaseout policy.

New Reactors Coming Online

Many countries have been planning to decarbonize for environmental reasons, and realize that they need reliable baseload power, which nuclear energy is primed to provide. After Russia’s invasion of Ukraine in February 2022, many European countries realized the issue with relying mainly on Russian natural gas and realized that nuclear power offered greater energy security.

These realizations have resulted in an increased appetite for nuclear reactors, and there are now 60 reactors under construction and another 110 planned globally, relative to 436 operating today, according to WNA. Notably, China accounts for a significant portion of these, with 24 under construction and 44 planned. China may be leading the development of new reactors, but significant demand is attributable to other countries due to reactor extensions and restarts highlighted in the previous point.

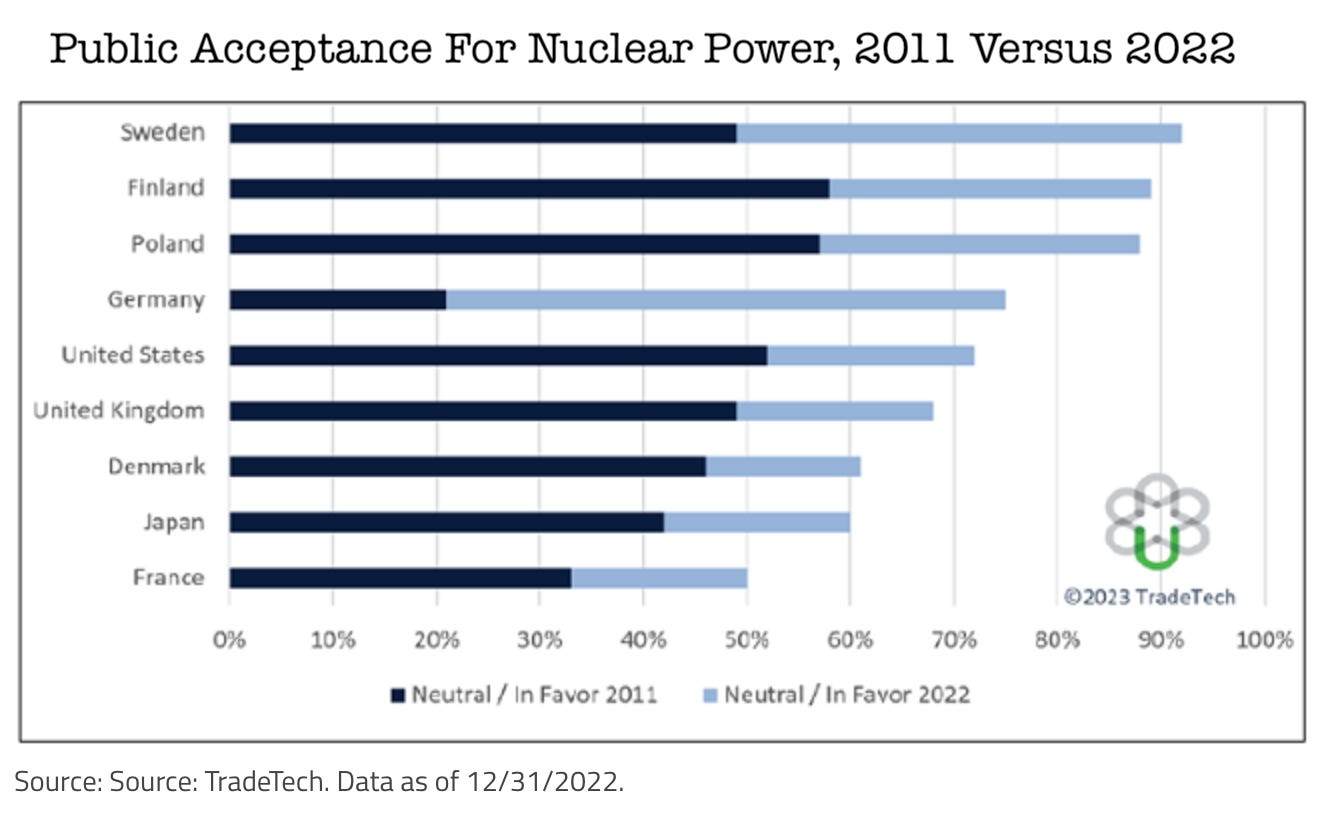

Overall, positive sentiment towards nuclear energy has been growing, and we believe it’s likely to persist this decade. With increased support for the nuclear industry, market participants will need to adapt to higher uranium demand and prices. Utilities may not be able to complacently draw down existing inventories in the hope that uranium prices will come down. The long-term demand and uncertain supply of uranium is very likely to support a sustained bull market for this asset class.

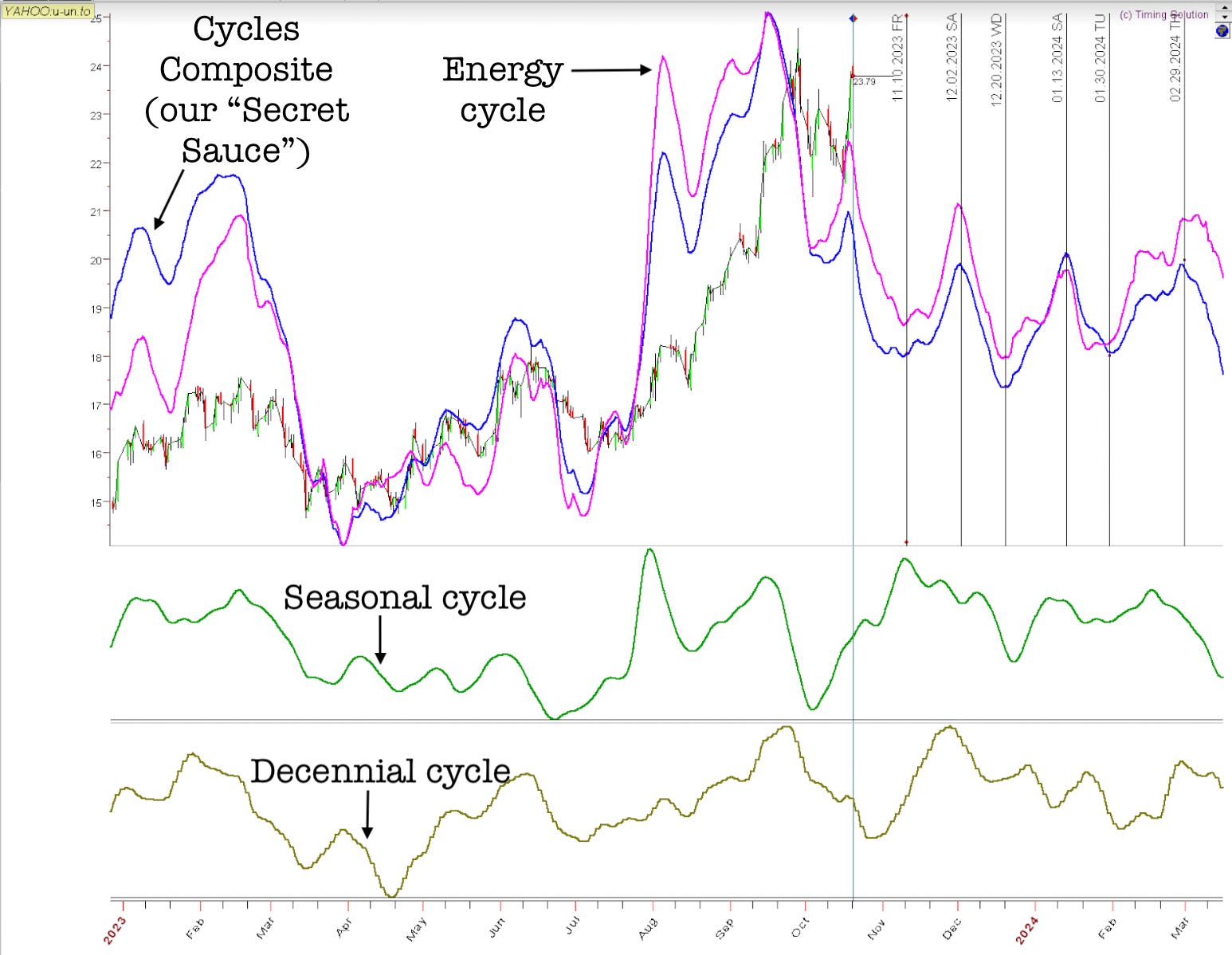

Cycles Point To Choppiness Until Q1 2024

Different Cycles for uranium point to a choppy/retracing uranium market until Q1 2024. This gives Cycles Edge enough time to share a little more about uranium’s developments over the years (important background knowledge) and look for attractive risk-reward setups for short and long term investors, so that we can help our subscribers Make Money through this promising asset class.

Next Uranium Article Background

From the start of the nuclear age in 1945 until 2019, the uranium industry has gone through 4 distinct periods. Each period has been unique in terms of its supply and demand, leading to big price swings that lasted for multiple years. The market has now entered its 5th major period, likely defined by persistent supply deficits. We’ll cover these 5 phases in the next uranium focused Commodities Piece, and following that we’ll regularly cover attractive uranium setups for our subscribers. Until next time!

Disclaimer - All materials, information, and ideas from Cycles Edge are for educational purposes only and should not be considered Financial Advice. This blog may document actions done by the owners/writers of this blog, thus it should be assumed that positions are likely taken. If this is an issue, please discontinue reading. Cycles Edge takes no responsibility for possible losses, as markets can be volatile and unpredictable, leading to constantly changing opinions or forecasts.