What is Acting Right

Premium Section: How to Trade the Best Areas of the Market

As we move deeper into earnings season, results—and more importantly, forward guidance—should help determine whether this breadth‑led leadership can carry the tape, or whether we slip back into a mega‑cap‑dominated regime (or perhaps a “Goldilocks” blend of the two).

Volatility spiked ahead of a critical “show‑me” stretch for AI and the Mag 7. Despite a late-week rally, the S&P 500 posted its first back-to-back weekly decline since June. Beneath the surface, the narrative was dominated by “TACO” headline whiplash, sharp divergence in semiconductors, and historic breakout in precious metals.

TACO Trade Turbulence

This week provided a masterclass on the “TACO Trade” (Trump Announces, Calls Off). As we outlined in our Tariff Playbook, institutions are increasingly treating these events as negotiation tactics rather than lasting policy shifts: volatility spikes into the early‑week selloff, then “smart money” steps in ahead of the inevitable de‑escalation.

The Setup: On Tuesday, the market slid on threats of 10% tariffs against eight European nations tied to the Greenland acquisition dispute. Notably, risk‑off flows pushed the S&P 500 and Nasdaq briefly negative for the year as traders swiftly repriced trade and growth risk.

The Reversal: By Thursday, a “framework deal” with NATO led to a quick reversal of these threats, triggering a sharp relief rally, particularly across cyclical and small-cap sectors most sensitive to trade and policy risk.

The TACO turbulence served as a testament to the market’s resiliency - even without the traditional “offensive” sectors (growth, tech) of the market performing well, a full TACO cycle was absorbed, and the primary uptrend still held. This suggests the market has broadened enough to sustain itself across various leadership regimes.

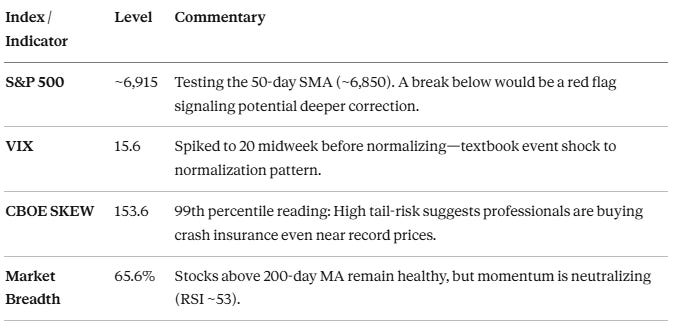

Technical Health Check

Despite the headline drama, the longer-term bullish posture remains intact, though the “wall of worry” is getting steeper. Here’s the technical snapshot:

The index sits above both the 50-day and 200-day moving averages, with the 50-day above the 200-day—maintaining a bullish longer-term structure. However, momentum indicators show consolidation rather than breakout energy.

More concerning is the elevated CBOE SKEW Index reading, which indicates that tail risk—the cost of protection against “black swan” events—remains high. Professional traders are buying insurance even as prices hover near records, suggesting institutional caution despite the market’s resilience.

With breadth continuing its uptrend, the Rotation Trade of 2026 continues. The breadth metrics, while still healthy, softened during the week’s selloff, and the NYSE Advance/Decline Line remains near overbought conditions that could prompt a pause.

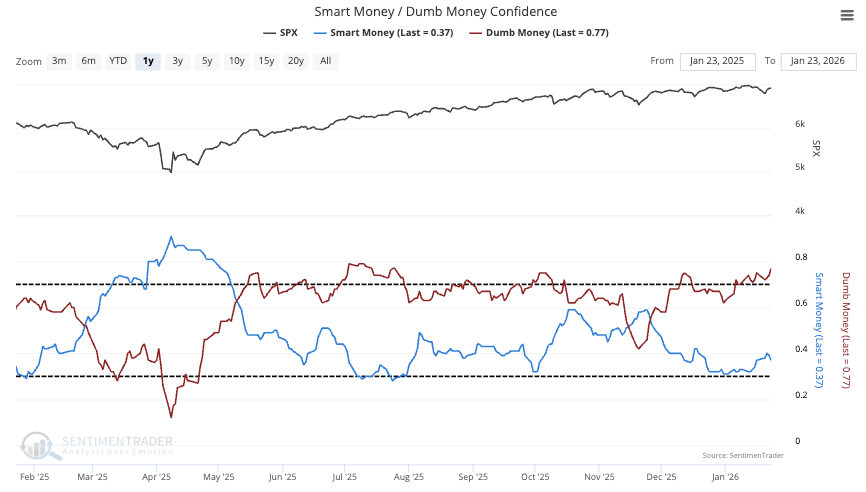

Sentiment continues to send a nuanced message. On one hand, Dumb Money remains highly engaged; on the other, Smart Money is cautious but starting to edge back in rather than staying completely sidelined. Current data confirms a striking gap in confidence levels.

Smart Money Confidence: Sitting near 0.37 (Institutional caution).

Dumb Money Confidence: Elevated at 0.77 (Retail exuberance).

Historically, when this spread widens to extremes, the market is prone to either a “pause that refreshes” or a sharp, short-term correction. The fact that Smart Money remains largely on the sidelines despite a 5.4% GDPNow forecast suggests they are more concerned about the Fed’s “sticky inflation” problem (Core PCE at 3.0%) and the upcoming leadership transition. Institutions are waiting for a “verification” of the macro picture before adding heavy exposure.

However, this divergence also creates opportunity. Any near-term weakness is likely to be met with institutional buying, as Smart Money has been waiting for better entry points. The charts show Smart Money beginning to dip its toes back in, which is a constructive development for the weeks ahead.

Sentiment is not yet frothy, as it climbs a steepening wall of worry. The model has climbed back to ~74 after a near-capitulation dip into the single digits in December, and remains under the euphoria threshold (~80)—a classic wall-of-worry profile with price holding up while sentiment is still catching up.

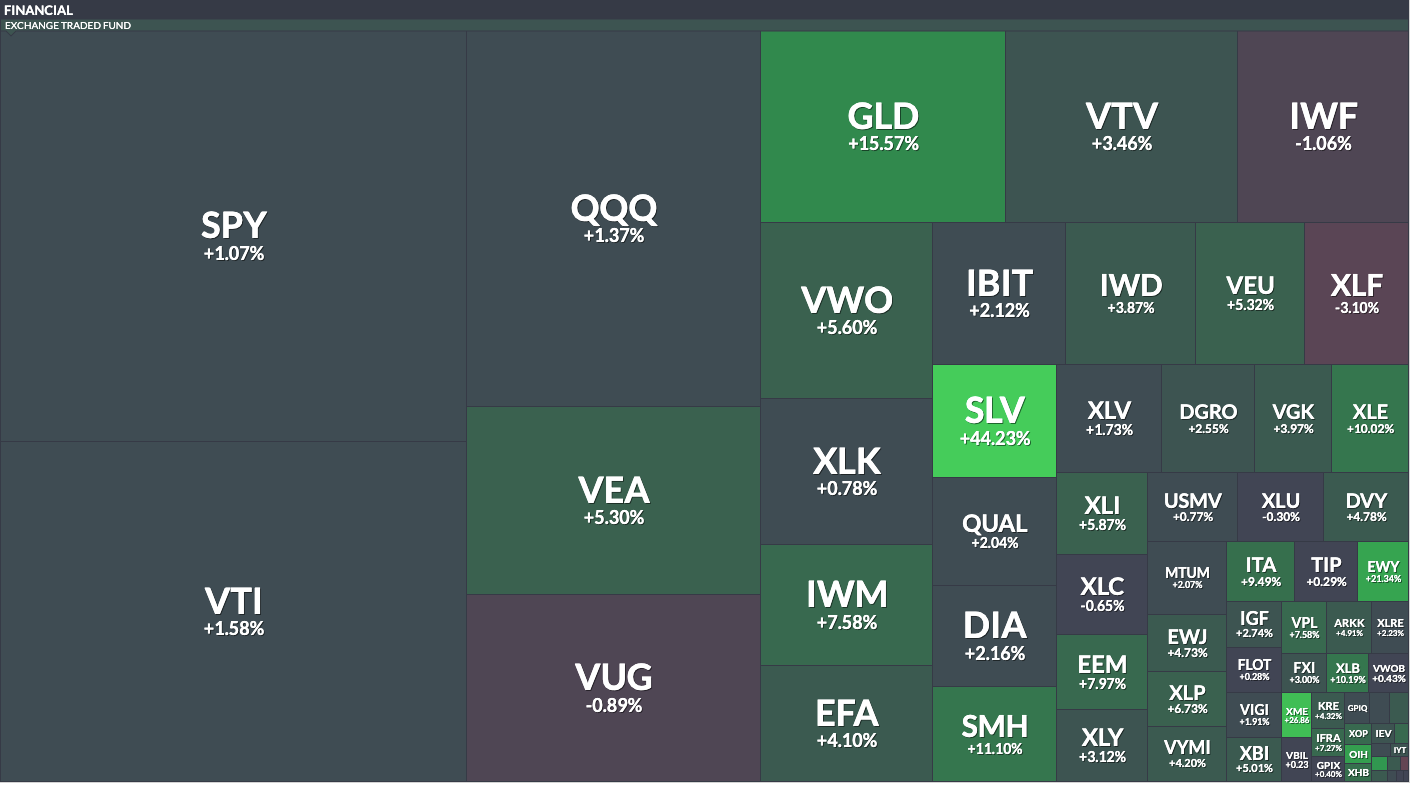

Precious Metals, International, Materials, Energy, Value, Industrials and Small Caps are leading the market. While leadership widens, the previous winners are creating a drag on the indices, with growth ETFs such as IWF (-1.1%) and VUG (-0.9%) struggling to keep pace. Notably, Financials (XLF -3.1%) weighed on the market due to the interest rate cap proposal (10% for one year) and following concerns over net interest margins

How to see areas of the market acting right? Notice the setup below with a split screen using the 4-Hour (4H) Chart. The 4H candle chart acts as a bridge between long-term structural trends and short-term execution. It provides enough “signal” to filter out short-term noise (5-15m timeframes), while remaining agile enough to enter into a swing trade before the daily chart even triggers. We like to use a split scree with the SPY in the lower chart for comparison.

Notice that the South Korea ETF (EWY) is acting right as it trends above the 15 SMA (blue). When the SPY pulled back hard, EWY went sideways…and when the SPY recovered, EWY outperformed and rose to new highs.

This is acting wrong…Software (IGV) is making lower highs and lower lows as the SPY is moving sideways. Notice that it often finds resistance on the 15 SMA, 30 SMA or 90 SMA before starting a new leg down.

In the Premium Section we’ll go over numerous ETFs acting right that have been money-makers for us this year.

Disclaimer - All materials, information, and ideas from Cycles Edge are for educational purposes only and should not be considered Financial Advice. This blog may document actions done by the owners/writers of this blog, thus it should be assumed that positions are likely taken. If this is an issue, please discontinue reading. Cycles Edge takes no responsibility for possible losses, as markets can be volatile and unpredictable, leading to constantly changing opinions or forecasts.