Fundamental Forces Behind Key Commodities – Commodity Piece

Coffee, Sugar, Cocoa, Cotton, Frozen Orange Juice

A short overview of why certain soft commodities are at or near new highs:

Cocoa

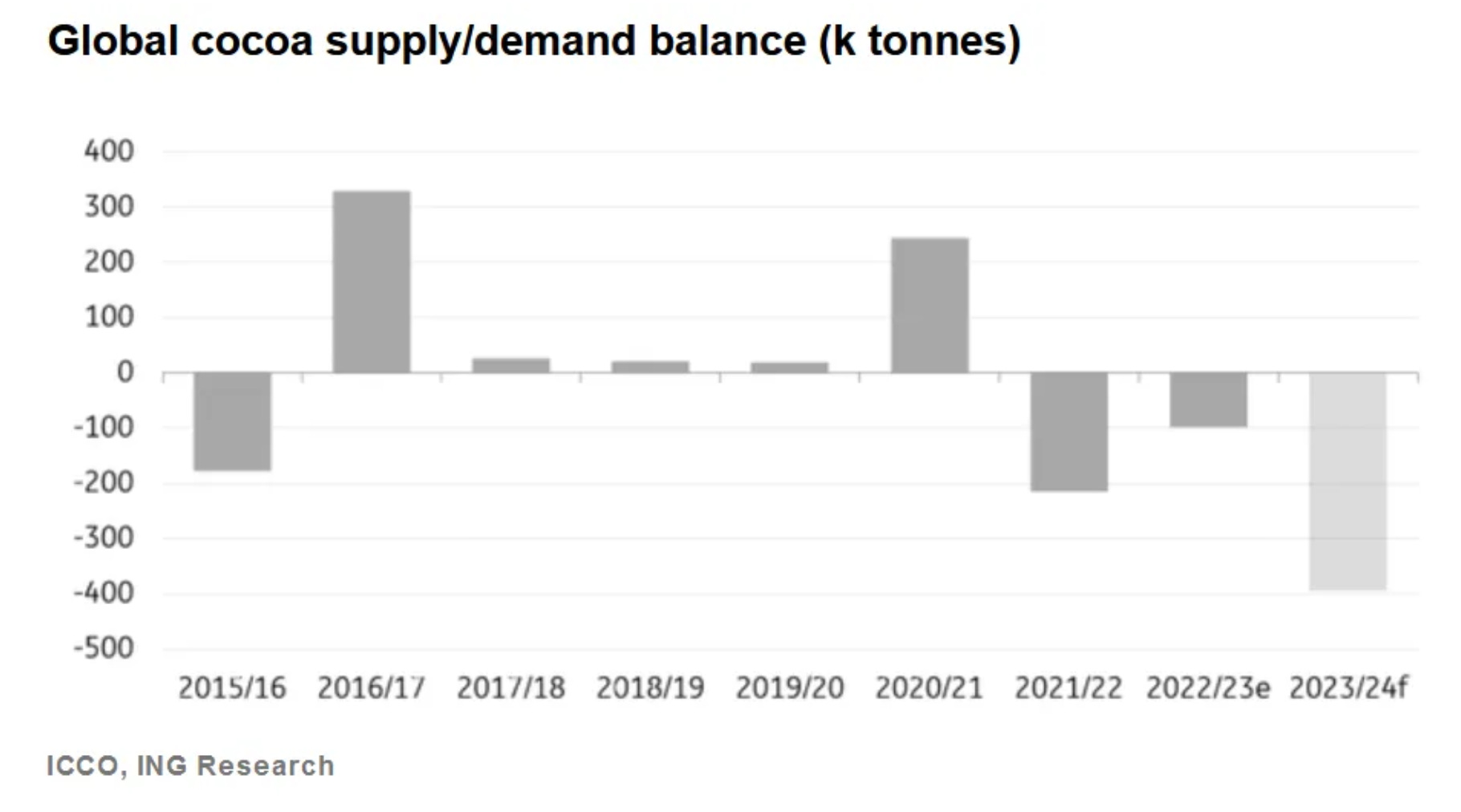

Cocoa has been on a melt-up. As per the International Cocoa Organization (ING), there was a deficit of 216kt in the global market during 2021 - 2022 and 99kt in 2022 - 2023. With a significant decline in West African output in the ongoing 2023/24 season, it is anticipated that the market will experience a substantial third deficit, nearing 400kt. This would result in cocoa inventory reaching its lowest levels in at least a decade. Moreover, it’ll be a bullish tailwind for cocoa, given that West Africa is responsible for three-quarters of the world’s cocoa produced.

Concerns are also arising regarding the potential impact on the 2024 to 2025 season. The cocoa regulator in Ivory Coast has reportedly suspended forward sales for the 2024 to 2025 season until there is more clarity on how the upcoming crop season might unfold, as stated by ING.

Coffee

Coffee prices are on the rise due to constrained coffee inventories and adverse weather conditions in Southeast Asia's coffee-producing areas, likely linked to El Niño. Additionally, rebel attacks on Red Sea shipping since early December have disrupted the supply chains between Vietnam, a leading Robusta producer, and European and US East Coast markets, further supporting prices.

Sugar

El Niño-induced dry conditions have led to reduced sugarcane harvests in major producers such as India and Thailand. In response to this, India extended sugar export restrictions in October to ensure sufficient domestic supplies. Thailand is experiencing the lowest yield from crushed cane in at least 13 years, primarily due to drought, while Brazil, the top producer, is also grappling with drought conditions. This has led to a sharp run-up in sugar prices.

Cotton

In the US, the leading cotton exporter, ending inventory for 2023 to 2024 reached a seven-year low due to consecutive years of drought affecting production. On a positive note, there is anticipation of a double-digit increase in cotton acres planted in 2024 compared to the previous year, as reported by Gro Intelligence.

Frozen Orange Juice

Furthermore, the higher prices for Orange Juice are expected to persist. The second-largest producer, the US, has faced challenges in production due to disease, extreme weather, and a decline in the number of Florida orange farmers. Florida's orange acreage has declined by more than half since 2000. As a result of these challenges, frozen orange juice prices have been going parabolic.

Fertilizer Prices

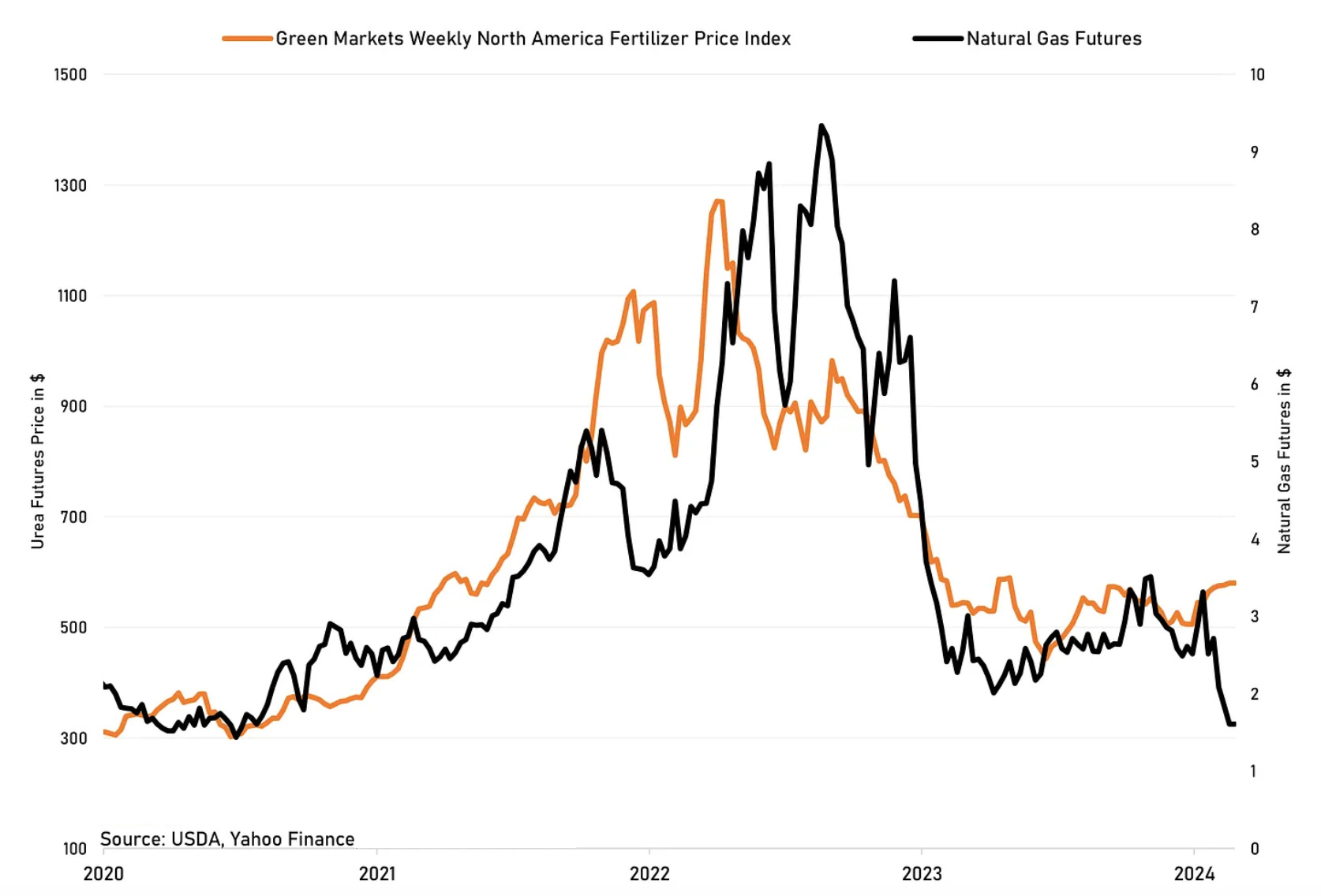

Fertilizer prices, although no longer at the peak levels seen in 2022, remain high when compared to historical standards. This is contributing to the sustenance of food inflation, as farmers incur increased costs to maintain the health of their crops.

Natural gas prices play a pivotal role in shaping fertilizer prices, acting as a fundamental determinant in the agricultural sector. The production of nitrogen-based fertilizers heavily relies on natural gas as a key input. Ammonia, a crucial component in nitrogen fertilizers, is synthesized through a process that involves significant natural gas consumption. Fluctuations in natural gas prices directly impact production costs, subsequently influencing fertilizer prices.

With natural gas prices putting in a significant bullish RSI divergence on the weekly timeframe + being at support, it strongly suggests the natural gas is highly probable to bounce here. This could be a bullish tailwind for fertilizer prices and stocks related to it.

Let us know in the comments below if there are any particular Commodities you would like us to cover in-depth. The next Commodity Piece will be focused on Silver (follow up from an earlier article on Gold and Gold Miners that can be found here). Until next time!